01-MAG UK.indd 1 11/07/05 13:45:45

As the public exchange offer closed on May 3

rd

, 2004,

the Group consolidated data for the first half of fiscal 2004-2005 are presented on the basis

of a 12-month consolidation of the Air France group (April-March) and 11 months for the KLM group (May-March).

Fiscal year 2003-04 is restated on a pro forma basis

01-MAG UK.indd 2 11/07/05 13:45:45

This reference document was filed with the French Autorité des marchés financiers on June 29

th

, 2005,

as required by Articles 211.1 to 211.42 of the general regulations of the AMF. It may be used to support

a financial operation if it is completed by an offering circular approved by the Autorité des marchés financiers

Contents

General

presentation

Activity report

Environmental and

employment data

Risks and risk

management

Financial report

Additional

information

As the public exchange offer closed on May 3

rd

, 2004,

the Group consolidated data for the first half of fiscal 2004-2005 are presented on the basis

of a 12-month consolidation of the Air France group (April-March) and 11 months for the KLM group (May-March).

Fiscal year 2003-04 is restated on a pro forma basis

01-MAG UK.indd 1 11/07/05 13:45:45

2

Chairman’s message

Dear Shareholders,

I

n creating Air France-KLM just over a year ago, we were

pioneers, almost like the first aviators. In some ways, we

reinvented the industry. By staying focused on customer and

shareholder satisfaction, we have opened up new opportunities

for our two airlines by creating the European and Worldwide

leader in air transport.

We have successfully implemented this project, already

producing a strong increase in results this year. A buoyant level

of activity in our three businesses, combined with an effective

cost-control policy, has enabled us to withstand the soaring

price of oil. Finally, thanks to the enthusiastic and effective

mobilization of the teams in both companies, to whom I pay

tribute, not only have synergies been implemented faster than

expected, but they have also been revised upwards.

This first successful year of the merger has been recognized

through various awards, notably from the American magazine,

Air Transport World, which voted Air France-KLM ‘Airline of the

Year’.

The reasons behind our success are simple: the co-operation

between our two companies is based on respect, commitment

and trust.

We view our cultural differences as advantages from which

we can benefit. At the same time, there are many things that

draw us together, fostering an environment of pragmatic co-

ordination, which has made it possible to launch a number of

joint projects, particularly in passenger and cargo but also in

maintenance and information systems. For our customers, this

merger has not only produced an enlarged network, greater

frequency of flights, and access to two efficient hubs, but has

also created a combined loyalty program, Flying Blue, a symbol

of our joint approach.

But just because our results were good this year, it doesn’t

mean we can stop here! To meet our objective of profitable

growth in the longer-term, there are numerous challenges

ahead.

The first and foremost is cost-control. It is by pursuing

the cost-control programs developed within both airlines

that we will succeed in creating an attractive offer, thereby

strengthening Air France-KLM’s leadership in an increasingly

competitive environment. Achieving the anticipated synergies

and identifying further ones will also be important factors in

keeping our costs down.

01-MAG UK.indd 2 11/07/05 13:45:45

3

In a sector exposed to rapid and deep-seated change, the

second challenge is to maintain the capacity to grow without

sacrificing the flexibility that has enabled us to adapt to the many

unforeseen events that have occurred since 2001. Building on

our two hubs, Roissy – Charles-de-Gaulle and Schiphol, we will

continue to develop our capacities in a focused and measured

way, by optimizing the complementary nature of the networks

and combining point-to-point traffic and connecting flights.

Our third challenge is to strengthen our financial structure

while continuing to generate sufficient cash flow to pursue the

rationalization and modernization of our fleet, which in turn will

improve our profitability and enable us to meet the demands of

sustainable development.

These challenges are not new, and we have proven ourselves

equal to the task in the past. Since its listing in 1999, your

company has evolved considerably. Back then, we ranked only

third in Europe with revenues of 10 billion euros, we were not

members of a major alliance, and we were state-owned. Now,

fully privatized, we are the leader in SkyTeam - the alliance

we have created with our key partners - and above all, we

have succeeded in carrying out the first merger in our sector

between two national airlines with different cultures.

In my view, our share price does not yet reflect this

transformation. The airline sector is often perceived as non

value-creating, but I would contend that few sectors could

have withstood the crises that have beset it since the terrorist

attacks of September 11 and their consequences. Our industry

has demonstrated its economic and social relevance and

its ability to weather difficult times. The industry will have to

face up to a difficult environment again this year. However, by

pursuing the strategic course that the Air France-KLM group

has adopted, we are confident that we will be able to achieve

our target of an operating result of a comparable level to that

of 2004-05.

Together with Leo van Wijk, Chairman of KLM, we share the

ambition of reinforcing our position as the World’s leading

airline group, for the benefit of our employees, customers and

shareholders, whose support over this past year has been

crucial.

Thank you for your continued support and the confidence you

have demonstrated in the Group,

Jean-Cyril Spinetta

Entrées de Chapitres UK.indd 5 11/07/05 13:47:55

G

eneral

6

Highlights

8

Key fi gures

10

Corporate governance

20

Stock market

25

Being a shareholder

presentation

Entrées de Chapitres UK.indd 2 11/07/05 15:31:17

28

Activity report

62

Environmental and

employment data

104

Financial report

202

Additional

information

82

Risks and risk

management

Entrées de Chapitres UK.indd 3 11/07/05 15:31:20

April 2004

On April 5

th

, Air France launches its exchange offer for KLM common stock. The shareholders

of KLM, at the Shareholders’ Meeting of April 19

th

, adopt the bylaw amendments allowing the

formation of the Air France-KLM group. On April 20

th

, the Air France Shareholders’ Meeting

approve the capital increase intended to remunerate the KLM shareholders.

May

The exchange offer for the KLM shares is highly successful, with 96.3% of the shares of

KLM common stock tendered in the offer. On May 5

th

, the Group is listed for trading in Paris,

Amsterdam and New York. On May 6

th

, the privatization of Air France is completed with the

transfer of the majority of the stock to the private sector by dilution of the French State’s stake.

On May 23

rd

, the portion of the vault in the embarkation room in terminal 2E at Roissy - Charles-de-

Gaulle collapses. All flights and personnel are reassigned to other terminals at the hub, resulting in

no cancellation.

June

The Group identifies the top three priorities for the coming years: implement the first measures

to generate synergies, continue a strict cost-control policy, and to develop the SkyTeam alliance.

July

The price of a barrel of oil (Brent IPE) rises above USD 40 in London, the highest level since 1990.

September

The Shareholders’ Meeting finalizes the legal structure of the Group with the creation of the

Air France-KLM holding company, which holds two air carrier subsidiaries: Air France and KLM.

KLM and its American partners Northwest Airlines and Continental join the SkyTeam alliance.

October

KLM celebrates its 85

th

anniversary around the theme Celebrating the spirit.

2004-05 Highlights

6

Entrées de Chapitres UK.indd 4 11/07/05 13:47:53

December

On December 9

th

, the French government reduces its equity interest from 44% to 23%, after the

sale of 47.7 million shares.

On December 26, a tsunami ravages the coasts of southern and southeast Asia, claiming

thousands of lives. The Air France and KLM teams are deployed to assist the survivors and

participate financially in the global aid effort.

January 2005

Air France-KLM is elected «Airline of the Year» by the American magazine Air Transport World.

Air France Cargo and KLM Cargo announce the creation of the European Cargo House,

an integrated management team in the cargo segment.

February

An offering reserved for Air France employees and a wage for share exchange are launched

following the French State’s sale of its stake in Air France-KLM.

Mars

Air France-KLM introduces Flying Blue, its single frequent flyer program, which replaces the

Fréquence Plus program from Air France and KLM’s Flying Dutchman program.

April

The price of a barrel of oil (Brent IPE) reaches a record of USD 56.51 in London.

May

At the end of the first successful year of the merger, the Group publishes substantially improved

results.

7

01-MAG UK.indd 7 11/07/05 13:45:52

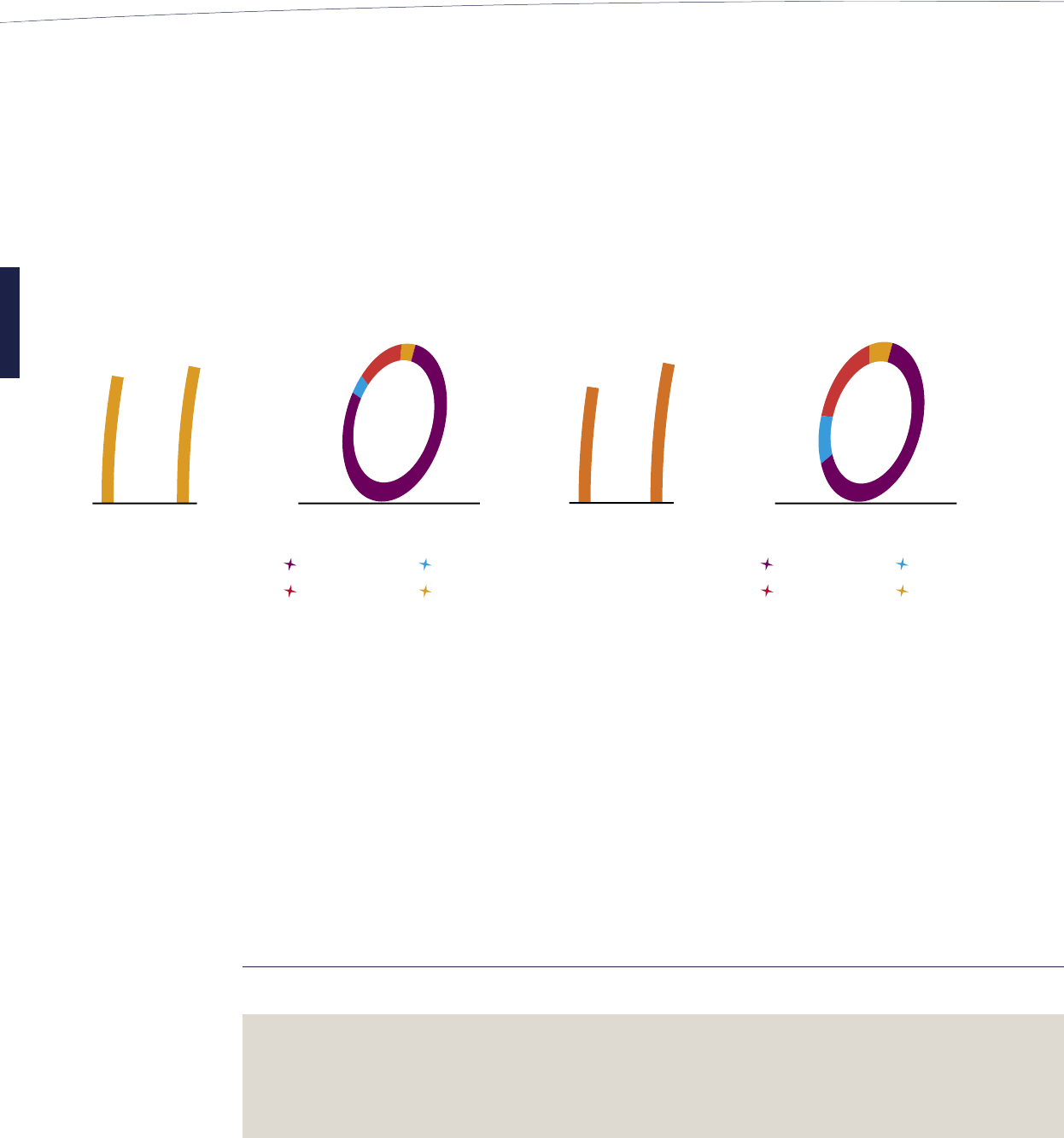

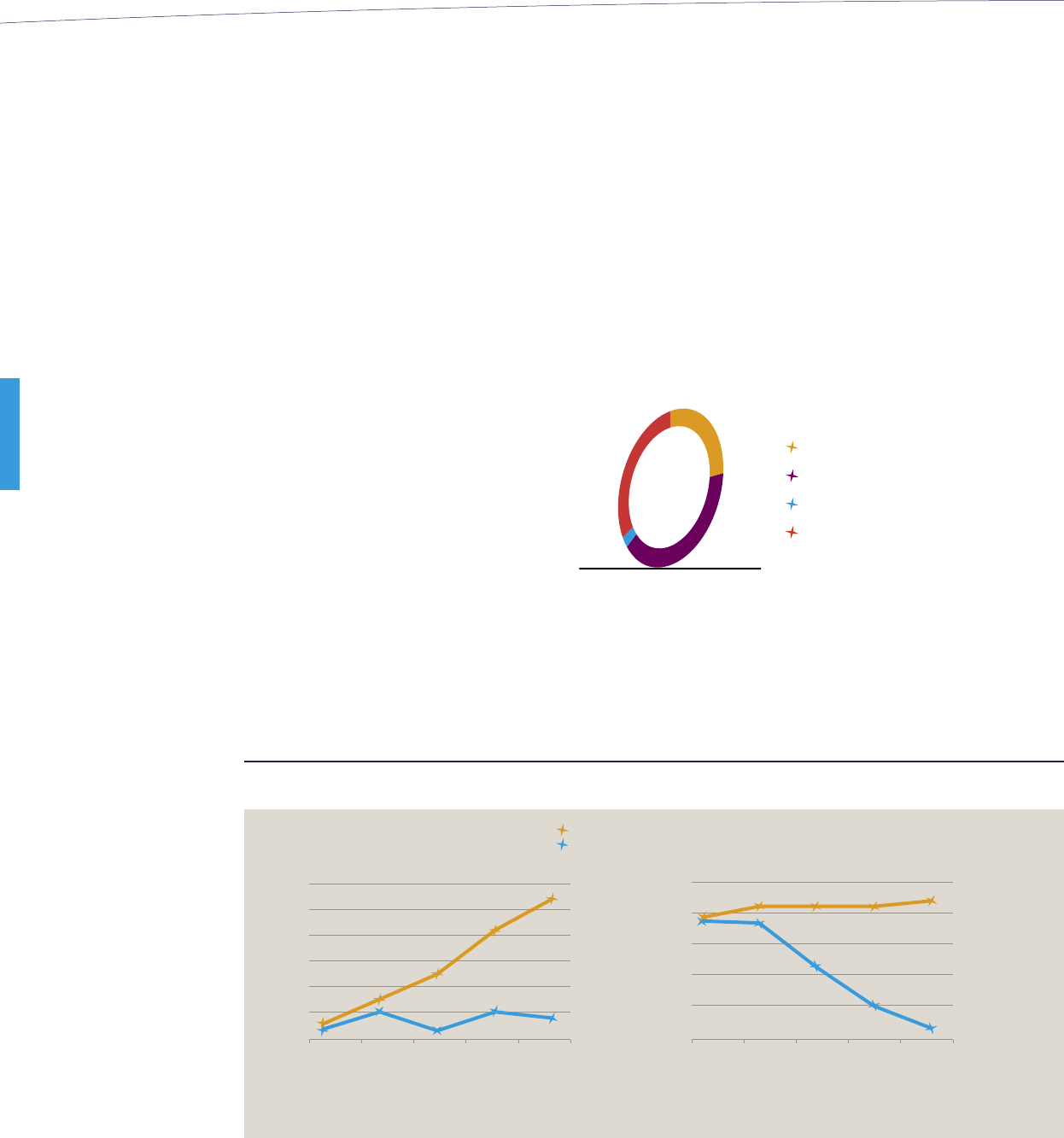

Key figures

The first year of the merger between Air France and KLM has been a resounding success. The teams

have worked together enthusiastically and the success of their combined efforts can be seen in the

115 million euros of synergies achieved, someway above the initial estimate of 65 million euros. They

have helped reinforce the cost-cutting programs at the two companies, enabling the Group to generate

strong growth in earnings despite the massive hike in oil prices.

A successful first year of the merger

2004-05

2003-04

pro forma

19.08

17.78

Cargo Other

Maintenance

Passenger

0.78

15.00

0.81

2.49

2004-05

2003-04

pro forma

489

405

Cargo Other

Maintenance

Passenger

48

312

34

95

Revenues

(in euro billion)

Breakdown

of revenues

(in euro billion)

Operating income

(before aircraft disposals)

(in euro million)

Breakdown of

operating income

(before aircraft disposals)

(in euro million)

All businesses made positive

contributions to operating

income, with a particularly

strong performance on cargo

(+61.0%).

Operating income before

aircraft disposals was up 20.7%

despite fuel costs rising 33.3%

to 2.6 billion euros.

Passenger and cargo activities

recorded growth of 6.8% and

9.4% respectively.

The Group’s revenues increased

7.3% thanks to a sustained level

of activity across all businesses.

8

01-MAG UK.indd 8 11/07/05 13:45:54

9

Consolidated figures

2004-05

2003-04

pro forma

351

292

Autres

Fret

Maintenance

Passage

12,34

12,34

12,3

4

12,3

4

Financing

Capital expenditure

2.19

2.13

5.90

1.21

5.55

1.06

March 31, 2004

March 31, 2005

pro forma

Net debt (in billions of euros)

Equity gearing

(net debt/shareholders’ equity)

in EUR million

2005

(1) (2)

2004

pro forma

(1)

Change

Revenues 19,078 17,782 +7.3%

EBITDAR 2,873 2,716 +5.8%

Operating income before aircraft disposals

489 405 +20.7%

Pre-tax consolidated net income

455 341 +33.4%

Net income, Group share 351 292 +20.2%

Earnings per share (in euro)

1.36 1.13 +20.4%

(1) Consolidation of Air France over 12 months (April -March) and KLM over 11 months (May-March).

(2) Consolidation of Servair over 15 months (January 2004-March 2005).

Net income,

Group share

(in euro million)

Capital expenditure

financing

(in euro billion)

Financial structure

(in euro billion)

The balance sheet structure has

been considerably strengthened

with equity gearing down to 1.06.

Capital expenditure on aircraft

totaled 1.8 billion euros and

ground investments 0.3 billion.

They were financed by 1.9 billion

in cash flow from operations and

0.3 billion in aircraft disposals.

Earnings per share came out at

1.36 euros at March 31

st

, 2005

compared with 1.13 euros the

previous year, while the dividend

is up to 15 euro cents (5 euro

cents at March 31

st

, 2004).

01-MAG UK.indd 9 11/07/05 13:45:56

Corporate governance

Board of Directors as at March 31

st

2005

The Board’s membership changed during fiscal year 2004–05

to take into consideration the merger between Air France and

KLM, which resulted in the privatization of the Air France group,

agreements signed by the two airlines relating to corporate go-

vernance, the transmission of holdings between the company

and its subsidiary and, finally, the sale of 25.5% of the capital

by the French State.

The Board, which had 21 members at March 31

st

2004,

increased to 26 members on June 24

th

2004, then reduced to

20 members at September 15

th

2004.

Finally, the sale of the French State’s interest in December 2004

resulted in a decrease in the number of its representatives on

the Board.

Since January 20

th

2005, there have been 16 members on the

Board of Directors:

• 11 members elected by the Shareholders’ Meeting;

• 2 representatives of the employee shareholders elected by

the Shareholders’ Meeting;

• 3 representatives of the French state appointed by ministerial

order.

First

appointed

Expiration date

of current term

of office

Number of shares

of the company’s

stock

Other directorships

Jean-Cyril Spinetta

Chairman of the Board

Born October 4

th

1943

23/09/1997

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

65,240

(excluding FCPE units)

Chairman and Chief Executive Officer

of Air France, Director of Alitalia and

Saint-Gobain, permanent represen-

tative of Air France on the Board of

Directors of Le Monde Entreprises.

Leo M. van Wijk

Vice-Chairman of the Board of Directors

Chairman of the Management Board

of KLM

Born October 18

th

1946

24/06/2004

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

500 Director of Northwest Airlines, member

of the Supervisory Board of Martinair,

Aegon N.V., Randstad Holding N.V.,

and member of the Advisory

Committee of ABN AMRO holding

and Kennemer Gasthuis.

Patricia Barbizet

Chief Executive Officer of Artémis

Born April 17

th

1955

03/01/2003

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

2,000 Chairman of the Supervisory Board

of Pinault-Printemps-Redoute and

member of the Supervisory Board

of Financière Pinault, Gucci, Yves

Saint-Laurent and Yves Saint-Laurent

Parfums. Director of FNAC, Christie’s

International plc. and TF1. Permanent

Artémis representative on the Board

of Directors of Bouygues, Sebdo

Le Point, and L’Agefi.

Giancarlo Cimoli

Chairman and Deputy Director of

Alitalia

Born December 12

th

1939

19/07/2004

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

10 Director of Enia S.p.A. and EnerTAD

S.p.A.

Directors appointed by the annual shareholders’ meeting

10

01-MAG UK.indd 10 11/07/05 13:45:56

11

First

appointed

Expiration date

of current term

of office

Number of shares

of the company’s

stock

Other directorships

Jean-François Dehecq

Chairman and Chief Executive Officer

of Sanofi-Aventis

Born January 1

st

1940

25/01/1995

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

523 Chairman and Director of Sanofi-Syn-

thelabo Daiichi Pharmaceuticals Co.,

Director Sanofi-Synthelabo Inc and

Fujisawa-Sanofi-Synthelabo.

Willem F. Duisenberg

Born July 9

th

1935

24/06/2004

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

100 Member of the Supervisory Board of

Rabobank.

Jean-Marc Espalioux

Chairman of the Management Board

of Accor

Born March 18

th

1952

14/09/2001

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

601 Director of Veolia Environnement and

Accor UK. Member of the Supervisory

Board of Club Méditerranée and per-

manent Accor representative on the

Supervisory Board of Groupe Lucien

Barrière SAS.

Pierre-Henri Gourgeon

Deputy Chief Executive Officer of

Air France-KLM

Born April 28

th

1946

20/01/2005

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2011

44,769

(excluding FCPE units)

Chief Operating Officer of Air France

and permanent representative of

Air France-KLM on the Board of

Directors of Air France, Chairman of

Amadeus GTD, Director of Autoroutes

du Sud de la France and Stéria.

Cornelis J. A. van Lede

Born November 21

st

1942

24/06/2004

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

1,000 Director of Reed Elsevier and Sara

Lee Corp. Chairman of the Supervisory

Board of Heineken, member of the

Supervisory Board of Akzo Nobel,

Philips Electronics and Air Liquide,

President of INSEAD.

Floris A. Maljers

Born August 12

th

1936

24/06/2004

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

500 Chairman of the Supervisory Board

of the Rotterdam School of Manage-

ment. Member of the Preferred Stock

Committee of DSM and member of

the Executive Committee of Rand

Europe.

Pierre Richard

Chief Executive Officer and Chairman

of the Management Board of Dexia

Born March 9

th

1941

20/10/1997

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

401

Chairman of the Supervisory Board

of Dexia Crédit Local, Vice-Chairman

of the Board of Directors of Dexia

Banque Belgium and Dexia Banque

Internationale in Luxembourg. Director

of Dexia Banque, FSA Holding, Crédit

du Nord, Le Monde and Generali

France. Member of the Board of Direc-

tors as expert advisor of the European

Investment Bank. Vice-Chairman of

the French Association of Banks and

member of the Executive Committee

of the French Banking Federation.

01-MAG UK.indd 11 11/07/05 13:45:58

First

appointed

Expiration date

of current term

of office

Number of shares

of the company’s

stock

Other directorships

Pierre-Mathieu Duhamel

Director of Budget, French Ministry

of the Economy, Finance and Industry

Born November 17

th

1956

15/01/2003

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

— Director of France Telecom, EDF and

SNCF. Official member of the CEA.

Jean-Louis Girodolle

Deputy Director with the Department

of the Treasury State Holdings Agency

Born August 2

nd

1968

24/06/2004

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

— Director of Renault, RATP, Autoroutes

du Sud de la France, and Aéroports

de Paris.

Claude Gressier

President of the Department

of Economic Affairs,

Counsel General for Public Works

Born July 2

nd

1943

24/06/2004

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

— None

The directors representing the French State are not required to hold shares of the company’s stock.

Directors representing the French State

First

appointed

Expiration date

of current term

of office

Number of shares

of the company’s

stock

Other directorships

Christian Magne

Representative of the ground staff and

cabin crews

Born August 20

th

1952

14/09/2001

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

172

(excluding FCPE units)

—

Christian Paris

Representative of flight deck crew

Born February 8

th

1954

14/09/2001

Shareholders’

Meeting called to

approve the finan-

cial statements for

the year ending

March 31

st

2010

28,000

(excluding FCPE units)

—

Directors representing employee shareholders

Secretary for the Board of Directors

Jean-Marc Bardy

Legal Counsel

12

01-MAG UK.indd 12 11/07/05 13:45:58

13

13

Board Organization and Operation

Directors are appointed for a six-year term of office. The minimum

number of directors’ shares is 10 shares for directors other

than those who represent the French State and employee

shareholders.

At its meeting on June 24

th

2004, the Board of Directors voted

not to separate the functions of the Chairman and Chief Executive

Officer. The Chairman is appointed by the Board of Directors; he

has full powers to manage the company, with the exception of

the limitations described below. The only limitations placed on the

powers of the Chairman and Chief Executive Officer are those set

forth in the internal rules of the Board of Directors, which stipu-

late that the Chairman and Chief Executive Officer must obtain

prior approval from the Board to conduct the following operations

when the amount exceeds 150 million euros:

• acquire or sell any interests in any companies formed or to be

formed, participate in the formation of any companies, groups

or organizations, subscribe to any issues of stocks, shares or

bonds;

• grant any exchanges, with or without cash payments, on the

Company’s assets, stocks or securities.

At its meeting of June 24

th

2004, the Board of directors decided

to appoint a Deputy Chief Executive Officer to assist the Chairman

and Chief Executive Officer, and defined his powers. The Deputy

Chief Executive Officer has extensive powers in economic, finan-

cial, commercial and employment matters. He must, however,

submit contracts of over 50 million euros for the signature of the

Chairman and Chief Executive Officer.

In addition to the laws and articles of association, the operations

of the Board are governed by internal regulations adopted by the

Board on June 17

th

2004.

These regulations define the roles of the four specialized Board

committees: the Audit Committee, the Strategy Committee, the

Compensation Committee and the Appointments Committee.

The Board of Directors has also adopted an ethics code that sets

forth the obligations of directors in terms of securities transac

-

tions, as well as a financial ethics code that defines the principles

with which the principal executives of the company responsible

for financial information and disclosure must comply.

Between three and five days before the meetings of the Board,

a file containing the agenda and any points that require special

analysis and prior consideration, summary memoranda and/or full

documentation is sent to Board members.

During fiscal year 2004–05, the Board of Directors met ten times.

The meetings lasted an average of three hours and the principal

items on the agenda were presented orally or by video, followed

by discussion. The attendance rate for directors was 80.7% (86%

in 2003–04).

The meetings of the Board were devoted to the review and/or

approval of the interim and final corporate and consolidated

financial statements, the budget, investments in the long-haul fleet,

the oil hedging policy, significant operations including changes

to the structures of the Group, the capital increase reserved

for KLM shareholders, the appointment and remuneration of

corporate officers and regulated agreements.

In its current form, the Board of Directors has initiated a self-

assessment of its operations, since March 31

st

, 2005

01-MAG UK.indd 13 11/07/05 13:46:00

Committees

This committee comprises 5 directors: Jean-François Dehecq,

Chairman of the committee, Jean-Louis Girodolle, Floris Maljers,

Pierre Richard and Christian Magne. The committee meetings are

also attended by the Vice President Finance of Air France-KLM,

the KLM Chief Financial Officer, the internal audit directors of each

of the two subsidiaries and the Statutory Auditors.

The committee has been tasked to review the consolidated

financial statements, the main financial risks, the results of in

-

ternal audits, the work programme, and the conclusions and

recommendations of the Statutory Auditors. The committee

approves the amount of the auditors’ fees and gives prior ap-

proval for some services provided by the Statutory Auditors.

It must also ensure the quality of procedures to ensure com

-

pliance with stock market regulations.

In addition, the Audit Committee reviews the interim and annual

consolidated accounts before they are submitted to the Board of

Directors and, specifically, it must review:

• the consolidation perimeter

• the relevance and permanence of the accounting methods

used to prepare the financial statements;

• the principal estimates made by management;

• the comments and recommendations made by the Statutory

Auditors and, if applicable, any significant adjustments resulting

from audits;

• with the company’s management a periodic review of the prin-

cipal financial risks and the off balanced sheet commitments;

• the programme and the results of the internal audits conducted

by the subsidiaries.

In fiscal year 2004–05, the Audit Committee met to review the

annual financial statements (May 12

th

2004), the half-yearly

statements (November 15

th

2004), and the quarterly state-

ments (February 14

th

2005). The Audit Committee also met on

September 21

st

2004 to review the 20-F document filed with

the US Securities and Exchange Commission and the process

to convert the annual financial statements of the company into

US GAAP because the company is listed on the New York

Stock Exchange. This meeting also dealt with the application

of the Sarbanes-Oxley Act to the company. Finally, on February

14

th

2005, the committee considered the progress on the

internal control action plan, and the internal audit work pro

-

gramme. The attendance rate for members was 81.7% (87.5%

in 2003–04).

The Audit Committee has the resources necessary to perform

its mission; it may also be assisted by persons outside the

company.

The Audit Committee

The Strategy Committee

The Strategy Committee comprises 7 directors: Jean-Cyril

Spinetta, Chairman of the committee, Leo van Wijk, Patricia

Barbizet, Pierre Duhamel, Claude Gressier, Christian Paris, and

Christian Magne.

The meetings are also attended by the Deputy Chief Executive

Officer, the Vice President Finance, and the Secretary of the

Board of Directors.

The committee has been tasked to review the strategies for

the Group’s business, changes in the structure of its fleet or

subsidiaries, the acquisition or disposal of aeronautical and

non-aeronautical assets, and the policy for air transport sub

-

contracting and alliances.

The committee devoted its November 8

th

2004 meeting to

preparing the Board’s work on the operations for modifying

Air France’s stake in Amadeus France and Amadeus GTD,

and concerning oil hedging policies. It reviewed the changes

in the Air France long-haul fleet plan during its meeting on

February 7

th

2005. The attendance rate for members was

100% (87.5% in 2003–04).

14

01-MAG UK.indd 14 11/07/05 13:46:00

15

The Remuneration Committee

The Appointments Committee

In the context of privatization, the company adopted rules for the

appointment of directors and corporate officers and, pursuant

to the agreements signed with KLM, the company wanted to

create an Appointments Committee, the internal rules of which

were approved by the Board of Directors on March 4

th

2004.

The committee has three members: Jean-Marc Espalioux,

Chairman of the committee, Patricia Barbizet, Jean-François

Dehecq, and one substitute member. The Appointments

Committee proposes candidates to serve as members of the

Board of Directors, which approves these recommendations

and submits them for election to the Shareholders’ Meeting

of the company. The Committee met in April 2004 to make

recommendations to the Board for the election of new Board

members by the Shareholders’ Meeting on June 24

th

2004.

The attendance rate for members was 100%.

The Appointments Committee also names the members of

the Strategic Management Committee after consulting the

Chairman and Chief Executive Officer of Air France for the

members who represent Air France and consulting the KLM

Supervisory Board for the members representing KLM.

The Remuneration Committee comprises 3 directors: Jean-Marc

Espalioux, Chairman of the Committee, Cornelis Van Lede and

Pierre Richard. It is primarily responsible for submitting proposals

for the level of and changes to the remuneration of the Chairman

and Chief Executive Officer.

It may also be called upon to give an opinion on the compensa

-

tion of senior executives, as well as on the policy for stock option

plans for new or existing shares.

The committee met on June 15

th

2004 and November 23

rd

2004

to give the Board an opinion on the variable portion of the

compensation for the Chairman and Chief Executive Officer for

fiscal year 2003–04 and to prepare for the Board’s discussions

on the compensation of the Chairman and Chief Executive

Officer and the Deputy Chief Executive Officer for fiscal year

2004–05. The attendance rate for members was 100% (100%

in 2003–04).

01-MAG UK.indd 15 11/07/05 13:46:01

The Remuneration Committee recommended to the Board of

Directors, which adopted the recommendation on November

23

rd

2004, that it set the elements of the compensation for the

Chairman and Chief Executive Officer and the Deputy Chief

Executive Officer for their duties in Air France-KLM and in

Air France as follows:

• Chairman and Chief Executive Officer: basic remuneration

of 750,000 euros p.a. over two years, with a bonus on ob-

jectives that can represent 60% of the basic remuneration.

- 2004-05: 550,000 euros and a target bonus of 60%

- 2005-06: 750,000 euros and a target bonus of 60%

• Deputy Chief Executive Officer: basic remuneration of

550,000 euros p.a. over two years, with a bonus on objec

-

tives that can represent 60% of the basic compensation.

- 2004-05: 370,000 euros and a target bonus of 50%

- 2005-06: 550,000 euros and a target bonus of 60%

The criteria for awarding the bonus are as follows:

• 50% linked to the achievement of the results set in the bud

-

get,

• 50% linked to the achievement of new strategic objectives,

including gains in market share and preservation of econo

-

mic balance.

The Chairman and Chief Executive Officer and the Deputy

Chief Executive Officer also have a pension plan, which was

set up in 2003 for 39 executives of Air France and guarantees

an annual pension benefit of between 35% and 40% of their

annual average remuneration during the last three years of

employment based on time with the company.

They do not receive a severance package if they leave the

company.

Compensation

The Shareholders’ Meeting of June 24th 2004 allocated

directors’ fees to the member of the Board for fiscal year

2004-05. The directors’ remuneration modalities are the

following: 12,000 euros as the fixed portion and 12,000 euros

as the variable portion; for the Committee Chairman:

10,000 euros for the Audit committee and 7,000 euros

for the other committees, for the Committee member:

6,000 euros for the Audit committee and 4,000 euros for

the other committees. A global amount of 553,028 euros

has been paid.

Compensation for Directors

Remuneration for Corporate Officers

(1) Amount transferred directly to the Treasury

Directors Directors’ fees paid by

the company

Pierre-Henri Gourgeon 4,849 euros

Claude Gressier 16,969 euros

Cornelis J.A. van Lede 17,878 euros

Christian Magne 32,500 euros

Floris A. Maljers 21,469 euros

Christian Paris 26,909 euros

Pierre Richard 29,636 euros

Directors who have left their

duties during the fiscal year 180,820 euros

Directors Directors’ fees paid by

the company

J

ean-Cyril Spinetta 31,000 euros

Leo M. van Wijk 22,060 euros

Patricia Barbizet 28,727 euros

Giancarlo Cimoli 9,091 euros

Jean-François Dehecq 35,818 euros

Pierre-Mathieu Duhamel 29,500 euros

Willem F. Duisenberg 15,878 euros

Jean-Marc Espalioux 30,364 euros

Jean-Louis Girodolle 19,560 euros

(1)

(1)

(1)

16

01-MAG UK.indd 16 11/07/05 13:46:02

17

2004-05 Position Gross

remuneration

Variable

remuneration

(1)

Achievement

of objective

Jean-Cyril Spinetta Chairman

and Chief

Executive Officer

of Air France-KLM

and Air France

550,000 euros 160,000 euros

100%

Leo van Wijk Director

Chairman of the

KLM Management Board

653,709 euros 429,731 euros

Partially

Pierre-Henri Gourgeon

Deputy Chief Executive

Officer of Air France-KLM

and Chief Operating Officer

of Air France

363,675 euros 142,300 euros 100%

(1) Variable remuneration received for the previous year.

Mr Spinetta and Mr Gourgeon have decided to part to the tran-

che offer to the group Air France employees and to exchange

salary for shares.

Stock options for new or existing shares granted to the

corporate officers of the company

The company has not established a stock option scheme for

its corporate officers.

For all information on the stock option schemes established by

the subsidiaries for their own executives, officers or employees

which entitle the holders to shares of Air France-KLM, see

«Additional Information – Information on the share capital

– Stock option schemes».

Loans and guarantees granted to corporate officers of

the company

None.

The remuneration of the Chairman and Chief Executive Officer

and the Deputy Chief Executive Officer of Air France-KLM is

invoiced to Air France under a regulated agreement approved

by the Board of Directors on November 23

rd

2004, for the

responsibilities they perform in this subsidiary.

The remuneration of the Chairman of the KLM Management

Board is decided by the KLM Supervisory Board. He also

benefits from a pension plan managed in accordance with

Dutch law. The company contributed 228,278 euros to this

plan for fiscal year 2004–05. In addition, Mr van Wijk may

benefit from a severance package equal to his final salary plus

an amount equal to the average of his bonuses for the last

three years if his contract is not renewed when it expires in

January 2007.

01-MAG UK.indd 17 11/07/05 13:46:04

Strategic Management Committee (SMC)

The Group is also managed by a Strategic Management Com-

mittee comprising eight members named by the Appointments

Committee. The SMC meets every two weeks, alternating

between Amsterdam and Paris, to make decisions relating in

particular to the coordination of networks and hubs, medium-

term budgets and plans, the fleet and investment plan and

alliances and partnerships.

The members of the SMC are paid by the companies to which

they are attached.

(For more information on the role and responsibilities of the

SMC and the Chairman of the SMC: see the section on

«Additional information».)

Jean-Cyril Spinetta

Chairman and Chief Executive Officer of Air France-KLM

and Air France and Chairman of the SMC

Joined the company in 1997

Born October 4

th

1943, Mr Spinetta attended the Ecole

Nationale d’Administration.

Leo van Wijk

Chairman of the KLM Management Board

Joined the company in 1971

Born October 18

th

1946, Mr van Wijk holds a master’s degree

in economics.

Philippe Calavia

Vice President Finance of Air France-KLM and

Chief Financial Officer of Air France

Joined the company in 1998

Born October 1

st

1948, Mr Calavia attended the Ecole

Nationale d’Administration.

Pierre-Henri Gourgeon

Deputy Chief Executive Officer of Air France-KLM and

Chief Operating Officer of Air France

Joined the company in 1993

Born April 28

th

1946, Mr Gourgeon attended the

Ecole Polytechnique.

Peter Hartman

Chief Operating Officer of KLM

Joined the company in 1973

Born April 3

rd

1949, Mr Hartman is a graduate in mechanical

engineering of the Polytechnical Institute of Amsterdam and a

graduate in management from the University of Rotterdam.

Bruno Matheu

Senior Vice President – Marketing and Network Management

for Air France

Joined the company in 1992

Born August 2

nd

1963, Mr Matheu is a graduate of the Ecole

Centrale de Paris.

Michael Wisbrun

Executive Vice-President for Cargo for KLM

Joined the company in 1978

Born March 14

th

1952, Mr Wisbrun holds a master degree in

engineering of the University of Delft.

Cees van Woudenberg

Chief Human Resources Officer, KLM

Joined the company in 1989

Born June 27

th

1948, Mr van Woudenberg is a law graduate

of the University of Leiden.

As of March 31

st

2005, the members of the Strategic Management Committee were

18

01-MAG UK.indd 18 11/07/05 13:46:04

19

From left to right:

Peter Hartman, Philippe Calavia, Jean-Cyril Spinetta,

Leo van Wijk, Cees van Woudenberg, Bruno Matheu,

Pierre-Henri Gourgeon, and Michael Wisbrun

01-MAG UK.indd 19 11/07/05 13:46:08

20

Stock market

Change in capital

Treasury stock

French State

Float Employees

32.1%

12.8%

54.0%

1.1%

At 31 March 2004

62.7%

11.7%

23.2%

2.4%

At 31 March 2005

62.7%

16.3%

18.6%

2.4%

At 11 April 2005

The capital of Air France-KLM is represented by 269,383,518

shares with a par value of 8.50 euros.

In May 2004, the French State’s interest was reduced to

44.1% further to the new equity issue reserved for KLM’s

shareholders, who contributed their shares to the offer.

In December 2004, the French State sold 47.7 million shares on

the stock market, reducing its stake in Air France-KLM to 23.2%.

In February 2005, the French State sold 8.4 million shares to

the employees of the Air France group in the offering reserved

for employees, and 12.6 million shares in the wage for share

exchange. These shares were delivered in March and April 2005.

Group shareholding structure at March 31

st

, 2005

AIR FRANCE-KLM

Publicly-traded company

100% of the capital

and voting rights

97.3% of the economic rights

49% of the voting rights

AIR FRANCE

KLM

Dutch

Foundations

Dutch

State

Other

shareholders

34.8%

of the voting rights

14.1%

of the voting rights

2.1% of the voting rights

2.7% of the economic rights

01-MAG UK.indd 20 11/07/05 16:06:21

21

Capital structure

To comply with the obligations of air carriers to monitor and

track their shareholders, Air France-KLM identifies its sharehol

-

ders. This operation has been performed every quarter since

the reduction in the State’s interest in December 2004.

Identifiable bearer shares (“TPI”) were analyzed on the basis of

thresholds that allowed the identification of 94.0% of the bea

-

rer shareholders (intermediaries holding a minimum of 141,000

shares and shareholders holding a minimum of 100 shares).

By adding in registered shareholders, the owners of 97.3% of

the capital were identified.

On the basis of the identifiable bearer shares, about 69% of the

Air France-KLM group is held by French shareholders and 21%

by European shareholders. On a corrected data base, the per-

centage of European shareholders drops to 14.7% in favor of

American shareholders, who increase to 13.1% of the capital.

Ownership and declaration rules

Any individual or legal entity, acting alone or with another, who

comes to hold directly or indirectly at least 0.5% of the ca

-

pital or voting rights of Air France–KLM or a multiple of this

percentage up to 5% is required to so inform Air France-KLM

by registered letter with return receipt sent within fifteen days

after the threshold is crossed.

For the rules concerning higher thresholds, refer to the chapter

«Information on the share capital».

On the basis of the thresholds defined above, the float breaks down as follows:

Number of shares As % of capital

Individual shareholders 27,938,595

10.4%

French institutional shareholders 58,083,677

21.6%

Non-resident shareholders: 75,889,407

28.2%

Including:

Great Britain 21,424,506

8.0%

United States

(1)

18,376,622 6.8%

Netherlands 13,879,235 5.2%

Belgium 9,466,276 3.5%

Luxembourg 7,146,610 2.7%

Switzerland 2,145,145 0.8%

Germany 1,239,055 0.5%

Other 1,670,754 2.2%

(1) including 9,019,294 ADS.

01-MAG UK.indd 21 11/07/05 13:46:10

The Air France-KLM share

Air France-KLM has been listed for trading on the Premier

Marché of Euronext Paris since February 22, 1999. Since

May 5, 2004, Air France-KLM has been listed on Euronext

Amsterdam and on the New York Stock Exchange in the form

of ADRs. Because it is listed for trading in the United States,

Air France-KLM publishes Form 20-F, which is available on the

Securities and Exchange Commission website (www.sec.gov).

A reconciliation document presenting the French and

US standards is made available to shareholders on the site

of Air France-KLM (www.airfranceklm-finance.com) or on

request by calling 33 1 41 56 88 85.

Euronext Paris

• ISIN Share Code: FR0000031122

• Reuters Code: AIRF.PA

• Code Bloomberg: AF PA

Euronext Amsterdam

• ISIN Share Code: FR0000031122

• Reuters Code: AIRF.AS

New York Stock Exchange

• Symbol: AKH et AKHWS

Included in the following indices

• Indices: NextCAC20, Euronext 100, DJ Eurostoxx, AMX

• Sector Indices: FTSE Cyclical services, FTSE Transport, FTSE Airlines & Airports

• Sustainable Development Indices: DJSI Stoxx 600, ASPI Eurozone, FTSE4Good

• Other: IAS (French Employee Shareholding Index)

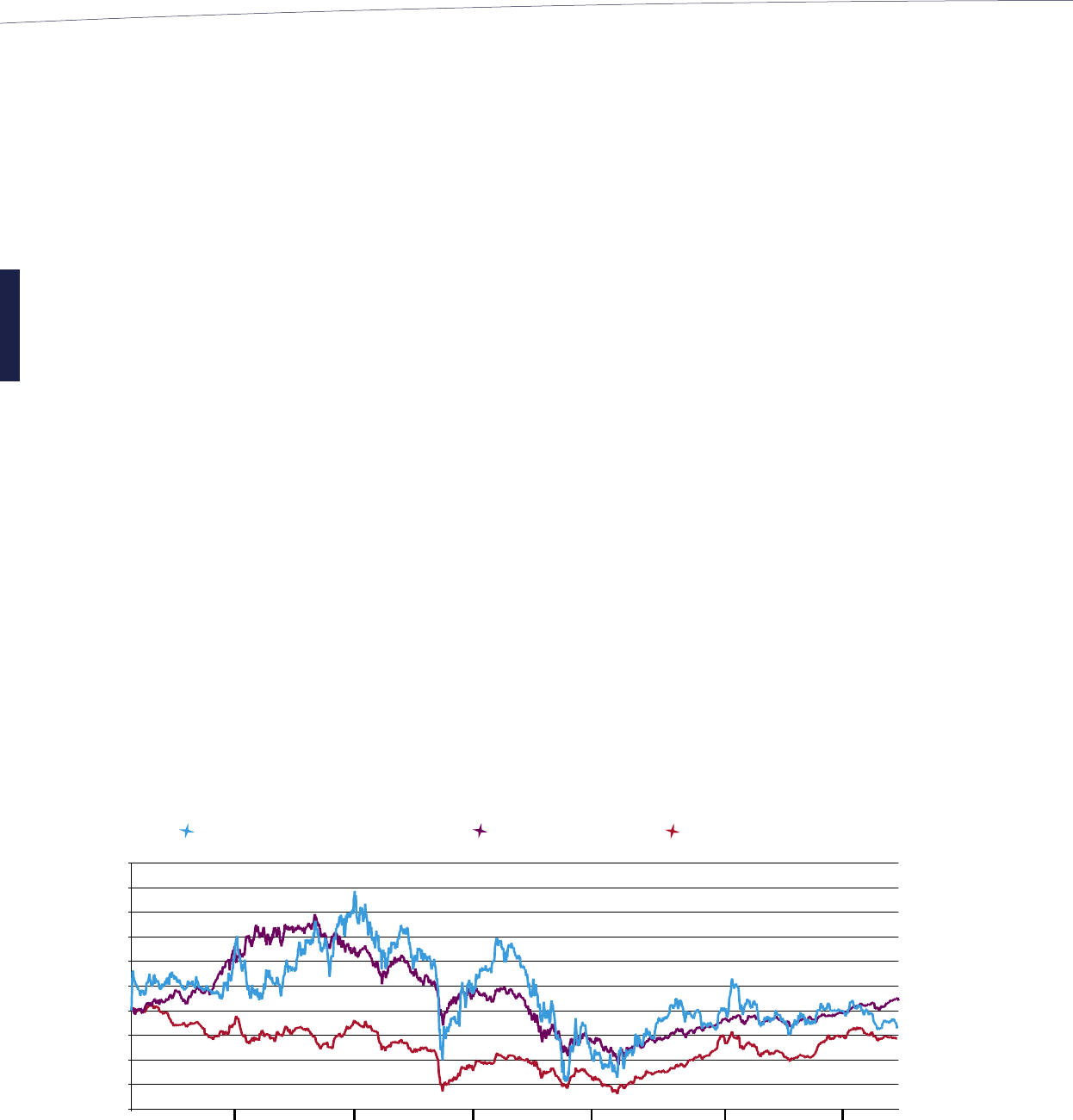

Air France-KLM share price

(Base 100 From February 19, 1999 to June 27, 2005)

40

55

70

85

100

115

130

145

160

175

190

1999

OP

F

2000 2001 2002 2003 2004 2005

SBF 120 (relative)

Air transport index (relative)

Air France-KLM closing

Securities Services

• In France, securities service and coupon payment is provided by Société Générale.

Société Générale: 32, rue du Champ de Tir-BP 81236, 44312 Nantes Cedex 3.

• In the Netherlands, securities service and coupon payment is provided by ABN AMRO.

ABN AMRO Corporate Finance: Gustav Mahlerlaan 10, 1082 PP Amsterdam.

• In the United States, securities service and coupon payment is provided by Citigroup.

Citigroup: 388 Greenwich Street, New York NY 10013.

22

01-MAG UK.indd 22 11/07/05 13:46:11

23

Trading

days

Average

Price (€)

Highest and

lowest price

(€)

Volume

Amount

(in € million

)

High Low

2003

November 20 13.37 14.17 12.14 10,866,525 143.9

December 21 12.60 13.06 12.04 8,861,787 112.6

2004

January 21 13.75 14.55 12.18 17,890,336 247.9

February 20 15.44 17.77 13.21 25,665,172 403.0

March

23 14.99 16.77 13.51 22,743,430 341.6

April 20 14.72 15.33 14.10 14,672,225 216.0

May 21 13.24 15.10 12.21 31,247,325 418.5

June 22 13.29 14.07 12.80 18,496,378 246.4

July 22 13.32 14.24 12.70 11,733,971 157.0

August 22 12.40 13.33 11.28 25,231,998 312.1

September 22 13.25 13.98 12.54 28,118,867 372.7

October 21 12.98 13.87 12.52 19,852,525 258.6

November 22 14.20 14.85 13.50 24,276,968 344.5

December 23 14.17 15.00 13.86 29,098,085 413.4

2005

January 21 13.89 14.27 13.36 28,041,883 389.0

February 20 14.52 15.14 13.98 33,033,615 481.6

March

21 14.13 14.66 13.53 28,962,252 409.0

April 21 13.17 14.02 11.98 35,195,326 464.0

Source: Euronext

Stock price and trading volumes

Equity warrants

Since May 2004, equity warrants (“BASA”) have been listed for trading on Euronext Paris and Euronext Amsterdam (ISIN BASA

Code: FR0010068965) and on the New York Stock Exchange (symbole: AKHW).

Bonds

Since April 22, 2005, bonds convertible and/or exchangeable to new or existing shares (OCEANE) of Air France-KLM have been

listed for trading on the Eurolist market of Euronext Paris. (ISIN Code: FR0010185975).

The FTSE4Good index includes more than 800 companies throughout the world, and measures their ac-

tions and initiatives in the areas of social responsibility and the environment. Inclusion in the FTSE4Good

should encourage socially responsible investment in the Group. This selection was announced at the end

of the evaluation conducted by the British organization EIRIS (Ethical Investment Research Service).

Air France-KLM included in the FTSE4Good index

01-MAG UK.indd 23 11/07/05 13:46:14

Fiscal year Earnings per share

(1)

(in euros)

Dividend

(in euro cents)

Amount after

tax credit

(in euro cents)

2001-02 0.70 10 15

2002-03 0.55 6 9

2003-04 0.43 5 7.5

2004-05 1.36 15 No tax credit

(1) by the average number of shares over the period.

Dividends paid

In accordance with the provisions of the 2004 French Finance

Law, which ended the system for avoir fiscal tax credits and

the précompte deduction of tax at source, the dividend paid

out for fiscal 2004-05 will not be associated with such a tax

credit. However, for individuals who are subject to income tax

in France, 50% of their amount will be incorporated into the

income tax base, entitling beneficiaries to a tax credit for all

dividends received of up to 115 euros for single, divorced or

widowed taxpayers and 203 euros for couples taxed jointly.

Furthermore, the amount distributed will be subject to an

exceptional deduction of 25% as an exceptional payment to the

French Treasury, which will be charged against or reimbursed

to corporate income tax at a rate of one-third per annum over

the next three years.

Air France won the second prize for employee shareholding in the SBF120 class. This prize, awarded by

the Federation of Employee Shareholders, Synerfil and the daily paper La Tribune, primarily recognizes

the quality of the savings plan, the information provided to employees, and the participation of employee

shareholders in the operations of the company.

Air France recognized for the development

of employee shareholding

24

01-MAG UK.indd 24 11/07/05 13:46:14

Tentative schedule for Air France-KLM publications for fiscal 2005-06

• Traffic figures: Around the fifth business day of every month

• First quarter results: September 2, 2005

• First half results: November 23, 2005

Shareholders’ Calendar

25

Being a shareholder

Air France-KLM is developing transparent, regular

and interactive information for its shareholders

Air France-KLM publishes monthly traffic figures for its passenger and

cargo activities and quarterly results, which are presented to the press

and financial analysts in a conference call or a meeting in Paris or London.

To present its financial results and the elements of its strategy directly, the

Group’s management regularly travels to meet with institutional investors

at roadshows in Europe, the United States, and Asia.

These quarterly results include financial notices published in the financial

and general press in France and the Netherlands. An eight-page letter to

individual shareholders written in French, English and Dutch is available

on the website. It is sent by mail or e-mail to the members of the

Shareholders’ Club.

In addition, for our employee shareholders, we provide educational

information that places the financial challenges and the group’s strategy

within its macro-economic environment. We offer these shareholders an

introduction to the way the stock market works, forums on themes related

to employee shareholding, a quarterly newsletter, a toll-free number, and

a website.

Air France-KLM has launched a new financial website:

www.airfranceklm-finance.com

Designed primarily for investors, analysts and shareholders, the site

offers the Group’s latest press releases (earnings, traffic, etc.), the

shareholders’ letter, the annual report and all the financial documents

published by Air France-KLM. www.airfranceklm-finance.com is

available in French, English and Dutch.

Regular information

01-MAG UK.indd 25 11/07/05 13:46:18

26

Information meetings for individual shareholders are held

regularly. During fiscal 2005-06, meetings will be organized

in Lille, Versailles, Nice, Nantes and Paris. Members of the

Shareholders’ Club who live in the regions visited will be invited

directly by letter.

Shareholders can obtain any additional information by calling

a toll-free number 0800 320 310 or 33 1 41 56 88 85 from

abroad.

Meetings with shareholders

Air France-KLM has created a Club for shareholders who hold at

least 50 shares of Air France-KLM. It has about 8,800 individual

shareholder members who receive Connecting, the quarterly

letter for shareholders, as well as the documents for the

Shareholders’ Meeting, whatever the method of shareholding.

As members of the Club, shareholders can participate in various

site visits. Offers from the Air France Museum are also regularly

available at preferential prices.

During the next fiscal year, the Club will adapt its communication

tools for individual Dutch shareholders who have joined the

Air France-KLM group.

Shareholders’ Club

In February 2005, Air France-KLM conducted a survey with members of its Club to find out

their reasons for becoming shareholders in the Group and their expectations for financial

information.

Over 800 people completed this survey and 96% of the respondents confirmed that they

have a positive image of Air France-KLM. More than 84% of the shareholders surveyed

indicated that they have held their shares since the initial public offering in 1999, and 36%

have purchased more Air France-KLM shares since then.

To learn about the Group, shareholders may consult the print press, the quarterly letter

Connecting and the annual report.

The top reason these shareholders invest in the Group is the image of the company, followed

by the prospects for growth, the value of the share, an interest in the air transport sector,

investment in a French company, and being an Air France-KLM customer

Shareholder survey - 96% have a positive image

of Air France-KLM

To adapt its financial communication to individual

shareholders’ expectations, Air France-KLM has established

an advisory committee representing individual shareholders

(“CCRAI”).

This committee, with 15 French members, meets an average of

four times a year and works on different projects, including the

website, the Shareholders’ Meeting, and the various financial

publications of Air France-KLM (annual report, letter to the

shareholders, etc.) The advisory committee has a page and a

mailbox on the website.

The CCRAI of Air France-KLM was restructured for fiscal 2004-05.

It will be opened to new Dutch representatives during the next

fiscal year.

Individual shareholders advisory committee

01-MAG UK.indd 26 11/07/05 13:46:18

Contact us

27

Every Air France-KLM shareholder, whatever the number of

shares, can participate and vote in the Shareholders’ Meeting.

Each share is entitled to one vote.

Registered shareholders receive all the information to

participate, vote or be represented at the Meeting, directly from

Société Générale, the agent of Air France-KLM.

Members of the Shareholders’ Club receive the documents

sent to registered shareholders, with the exception of the vote

card. These documents as well as the vote card are available

and can be downloaded on www.airfranceklm-finance.com

Bearer shareholders must contact their account manager to

ensure their shares are not transferable for the five days before

the date of the Meeting. They then receive their admission

cards or on request a form to vote or to give proxy by mail.

Admission cards for the Meeting are sent to any shareholder

on request directly, or via his or her account manager, no later

than six days before the date of the meeting by registered mail

with return receipt from the Société Générale.

Shareholders who cannot attend the Shareholders’ Meeting can:

- give their proxy to the Chairman; they just have to send in the

form to vote by mail or by proxy;

- be represented by their spouse or another shareholder;

- vote by mail. Forms to vote by mail can be obtained from

Société Générale. These forms will be counted only if they

reach Société Générale at least three days before the

Meeting.

Contact: Société Générale

Département Titres et Bourse

32, rue du Champ-de-Tir – BP 81236

44312 Nantes Cedex 3

Participate in the Shareholders’ Meeting

by telephone

From France, call 0800 320 310 (toll-free number) – Monday through Friday, from 10:30 a.m. to 12:30 p.m.

and from 2:30 to 5:30 p.m.

From abroad or the French Overseas Territories and Departments, call +33 1 41 56 88 85.

by mail

Air France-KLM

Shareholder Relations

DB-AC

45, rue de Paris

95 747 ROISSY - CDG Cedex

on the Internet

A suggestion form is available on the website www.airfranceklm-finance.com, under Contacts.

For shareholders who want to record their shares as registered

shares, Air France-KLM has appointed Société Générale.

By opting for this form of shareholding, shareholders are not

charged for custodial and management fees.

Société Générale offers registered shareholders of

Air France-KLM interactive services so that they can view

their assets, be informed of transactions made on their

securities account, and place market orders. These services

are accessible by phone, via the Nomilia voice server at

+33 825 820 000 or on the Internet.

Registered shareholders

Entrées de Chapitres UK.indd 9 11/07/05 13:47:59

A

ctivity

report

30

Strategy

36

Market and competitive environment

40

Passenger activity

45

Cargo activity

48

Maintenance activity

50

Other activities

52

SkyTeam

56

Air France-KLM group fl eet

Entrées de Chapitres UK.indd 6 11/07/05 15:40:55

104

Financial report

202

Additional

information

82

Risks and risk

management

62

Environmental and

employment data

Entrées de Chapitres UK.indd 7 11/07/05 15:40:58

Your group is the European leader in air transport. Can

you talk to us about the sector, which seems to have

been beset by many crises?

Jean-Cyril Spinetta

Before answering your question, I would like to emphasize

the important role played by the air transport sector within

our economy. Air transport exists because it fulfills both an

economic and a social demand.

Air transport is a necessity for business, and it serves

the economy. In France, more than one out of every two

passengers travels for business reasons, thereby developing

solid international ties with different markets. According to

a recent report, the air passenger market has grown at an

average rate of 5% over the last ten years, while cargo has

risen by 6 to 7%. This dynamic growth contributes to GDP

growth and job creation: in France, 400,000 jobs are related

directly and indirectly to the air transport sector.

Air transport also meets the social requirement for mobility,

while contributing to opening up and developing the country.

Regrettably, these social and economic benefits are not always

emphasized in the debates about the development of air

transport; too often, it is the negative aspects which receive

the most attention.

Air transport also actively contributes to the international

profile of France. Although it represents only one percent of

the world’s population and 4% of global GDP, France accounts

for 100 million passengers annually or 6% of the World total. It

is also worth remembering that tourism is the World’s largest

industry, and that France is its leader. Foreign tourists visiting

France, who are highly dependent on the airline industry, spent

on average 85 million euros a day in 2003.

Leo van Wijk

Air transport also plays an important role in the Dutch economy.

The position of the Netherlands in air transport is much more

significant than one might expect of a nation of 16 million

people. The Dutch Ministry of Transport recently identified over

120,000 direct and indirect jobs generated by Schiphol Airport.

In addition, the easy air accessibility of the Netherlands has

greatly contributed to the competitiveness of our economy

over the last few decades, facilitating the establishment on our

soil of leading companies in many sectors. For our country, air

transport is a source of national pride, and KLM contributes to

that pride.

What are the cornerstones of your strategy?

Jean-Cyril Spinetta

The strength of the Air France–KLM group is that it is founded

on two of Europe’s largest hubs – Paris and Amsterdam – which

both have strong growth potential.

Moreover, taking Europe and its requirements in terms of

relations with the World’s other major economic regions in the

future, it becomes apparent that there is still enormous scope

for development, particularly in connecting traffic.

Paris and Amsterdam are two of the three or four European

airports best positioned to take advantage of strong demand

in decades to come. That is why our strategy is firmly based

around the development of these two hubs, which each have

the possibility of further expansion while competing platforms

are nearing saturation.

Strategy

Interview with Jean-Cyril Spinetta and Leo van Wijk

30

Entrées de Chapitres UK.indd 8 11/07/05 13:47:57

31

Leo van Wijk

In addition, our hub system will help us to take advantage of

the opportunities created by the expansion of the European

Union to the East. Most of the countries that have joined the EU

are relatively small, and have already indicated that they will not

be developing major airport infrastructures. As a result, they will

have to rely on existing hubs such as Paris or Amsterdam.

Moreover, European countries having, historically, restricted

access to their markets, have created the conditions for the

strong development of point-to-point traffic. Today, the Group

is well positioned to combine point-to-point and connecting

traffic.

Is this multi-hub system, which connects the platforms

of Roissy – Charles-de-Gaulle and Schiphol 15 times a

day, profitable?

Jean-Cyril Spinetta

Yes! Not only does the multi-hub system enhance our control

over the costs at each company by streamlining our networks

- which we could not have done without each other - but it

also generates excellent revenues, thereby improving our

profitability.

Some people make the distinction between point-to-point

traffic, which supposedly generates higher revenues, and

connecting traffic, which is regarded as having lower revenue

levels. However, the figures show this is not the case. Last year,

we carried 9% more passengers, even though our offer rose

by only 7%. Our load factor, at 79%, was higher than that of

any of our main competitors. This benefited our unit revenues,

which were up 1.6%. So, as you can see, our multi-hub system

is definitely profitable.

Leo van Wijk

Connecting traffic also has a bright future. In 2004, on the

Europe-North America routes, 56% of passengers were

connecting passengers. This figure was as high as 63% for

Europe-Asia connections. Moreover, according to various

studies, by 2013 the industry is expected to carry approximately

215 million passengers on intercontinental flights, including 115

million connecting passengers. This data justifies and supports

our strategy.

Moreover any increase in point-to-point traffic tends to have

a greater impact on the smaller hubs. Having two of Europe’s

largest hubs within our Group is, therefore, a clear advantage.

We must build on our assets: the two hubs must remain

attractive on the strength of the multiple destinations and the

frequency of the flights they offer. Developing one of the hubs to

the detriment of the other would create imbalances that would

heavily penalize the entire group. One of the main challenges

for our alliance involves balancing growth between KLM and

Air France.

Air France-KLM seems to have ambitious capacity growth

targets of around 5% per annum. Isn’t this risky when

there is a great deal of talk about excess capacity?

Leo van Wijk

I think it is important to emphasize that the Group has

responded to market demand. For the year just ended, the rise

in traffic exceeded that of our offer. Moreover, our load factor

is the highest in Europe. This is reinforced by the statistics

from the AEA showing that traffic has increased faster than the

offer. Currently, we are not witnessing any excess capacity in

Europe.

01-MAG UK.indd 31 11/07/05 13:46:23

Jean-Cyril Spinetta

Given the outlook for World growth, we expect to grow our

offer by 5% per annum in the next few years, slightly below

projected demand. More specifically, we intend to focus on

expanding long-haul traffic, mainly to high growth markets like

Asia and Latin America.

At the same time, we will maintain our flexibility in order to be

able to confront the risks inherent in our sector. The flexibility of

our offer is the result of our balanced network, which provides a

natural hedge against geopolitical and economic risks. Neither

Air France or KLM have ever developed «niche» networks,

and as a result we are not dependent on any single zone. This

balance is a safety factor in our strategy of profitable growth.

Is Air France-KLM synonymous with benefits for your

customers?

Jean-Cyril Spinetta

Of course there are many advantages to being an

Air France-KLM customer. First, the co-ordination of our hubs

at Roissy – Charles-de-Gaulle and Schiphol has enhanced our

network by increasing the range of destinations and connecting

flights. Our passengers now benefit from an expanded schedule

to over 234 destinations, one of the largest networks in the

world. The multi-hub system has therefore made us stronger in

a number of markets.

Second, we have been innovative by allowing passengers to

combine fares. Passengers can select which of the two airlines

offers the best schedule, and swap airline for the outbound

and inbound flights, while maintaining the benefits of a round-

trip fare. So, the competitiveness of our offer has increased,

and our passengers seem to appreciate the flexibility. It is no

longer up to the customer to fit around the airline’s schedule,

but up to the airline to adapt its schedules to the customer’s

requirements!

Leo van Wijk

We have just launched Flying Blue, our joint customer loyalty

program which offers significantly enhanced benefits compared

with the old Fréquence Plus and Flying Dutchman programs.

Now, ten million passengers are able to enjoy the tangible

benefits our alliance. We are also developing our e-services in

order to facilitate booking and check-in with both Air France

and KLM.

You generated 115 million euros in synergies last year,

surpassing your initial target. You have forecast

280 million euros for 2005-06 and more than double

that figure – 580 million euros – by 2008-09. How do you

explain the speed with which you have implemented

these synergies?

Leo van Wijk

With regard to synergies, we have only just started. The

synergies between Air France and KLM will continue to be a

major source of cost-savings in the coming years.

Until now, most of the synergies have been in revenues, although

some cost synergies have been generated. We have mainly

focused on optimizing our respective networks, selecting to

concentrate our flights to certain destinations on the one of our

two hubs which made the most economic sense. Take Caracas

for instance: the final destination for traffic out of Amsterdam

was primarily Southern Europe. Therefore, Paris was the more

logical hub, particularly since this wasn’t a profitable flight for

us. On the other hand, the final destination of most passengers

from Manila was Northern Europe, making Amsterdam the best

solution. This issue also arose when we opened the route to

the new Japanese airport at Nagoya. Should we both fly there

separately, running the risk of excess capacity? In the event,

we decided to offer this destination from Paris only.

32

01-MAG UK.indd 32 11/07/05 13:46:24

33

Gradually, there will be a rebalancing towards cost synergies

and, in five years’ time, the breakdown should be some 60%

for revenue synergies and 40% for cost synergies.

In the course of working together, we have also discovered

new sources of potential synergies that will be implemented

over the coming years.

Jean-Cyril Spinetta

If synergies are being realized faster than projected, this is

because the work of both teams is being undertaken with the full

co-operation of all involved and without hesitation on either side.

We are delighted by this. One of the factors often underestimated

in merger situations is the importance of employee support for

the process. Many mergers have failed because insufficient

attention was paid to employee motivation during the integration

process. In a service industry such as ours, this could have

a particularly devastating effect, and we could easily destroy

many of our opportunities.

In this context, it was crucial to us that our teams work together.

Joint counters were installed, notably in our two hubs at Schiphol

and Roissy – Charles-de-Gaulle; projects are underway in cargo,

maintenance and information systems. Flying Blue, our combined

customer loyalty program is a great example.

We are supporting this co-operation, going beyond cultural

differences. Not only are we not in a hurry to make them disappear,

we positively want to turn them to our advantage. We are learning

from each other and as a result, becoming stronger, more

competitive and more efficient. An exchange for some dozen young

French and Dutch managers from both Air France and KLM took

place from April to June. I found their enthusiasm impressive.

What gives us the most confidence in our decision to merge

our two companies is that, over time our approach has become

increasingly recognized by our employees as being “the right

thing to do”.

In September, KLM and its American partners Northwest

Airlines and Continental joined the SkyTeam alliance.

What role do you see this alliance playing in your

strategy?

Jean-Cyril Spinetta

Alliances are playing an important role in a process of

consolidation in the sector that appears inevitable and

necessary. I believe that the future of the alliance system,

particularly between European and American companies,

will undoubtedly see stronger ties among the various

players. The example of Northwest Airlines and KLM is a

case in point: in Europe, it is clear that the Air France-KLM

model offers an effective response to the complex issues

facing the industry. One of our competitors has already

been inspired by it!

Leo van Wijk

Today, SkyTeam is the world’s second-largest alliance in terms

of passengers, and the number one in cargo following the

inclusion of KLM and its American partners. We are also the

leading alliance on the North Atlantic route, which offers some

interesting prospects.

We are getting ready to welcome Aeroflot and China Southern,

which have signed letters of intent and are expected to

join the alliance by the end of 2005. This will significantly

enhance our presence in the Russian and Chinese markets,

enabling the implementation of code-sharing on domestic

and regional lines.

Within SkyTeam, we have also created the status of associate

member for companies that were previously linked to

Air France and KLM.

01-MAG UK.indd 33 11/07/05 13:46:26

Controlling costs has been a priority at Air France and

KLM for several years now. How do you intend to reduce

your costs in a context of rising fuel and tax charges?

Jean-Cyril Spinetta

There are ambitious programs at both Air France and KLM

aimed at permanently reducing costs to enable us to withstand

the brutal rises in fuel, tax and royalty charges.

For fuel, we have developed an effective hedging policy.

As far as taxes and royalties are concerned, we must make

those who set these charges understand that increasing them

further will be extremely damaging for the European operators.

These taxes seem to be rising inordinately at a time when the

airline industry as a whole is going through a period of economic

turbulence.

Nevertheless, I remain optimistic, even if there is still a long way

to go. Take the air navigation royalties that we pay in respect

of Air France, which fell in 2004 and will continue to be reduced

in 2005. This illustrates a growing awareness of the need to

reduce many of these taxes.

Leo van Wijk

It is wrong to believe that there are no alternatives than to travel

through Paris, Amsterdam, London or Frankfurt. If European

airports continue to ignore the issue of airport transit costs, we

could see airlines make a shift towards less expensive airports,

even outside Europe.

Another issue is security-related costs. We pay them of course,

but at the same time we are vigilant to ensure that the measures

taken are effective and realistic. If we believe they do not meet

these two criteria, we will seek to remedy them, in co-operation

with other air carriers within the AEA or IATA.

Jean-Cyril Spinetta

But at the end of the day, these issues must not distract us from

our prime objective which is to improve our competitiveness

and to reduce those costs over which we have direct control.

If we are unable to offer our customers fares of a level they are

prepared to pay, we will be literally swept away. Therefore, the

main priority is to reduce costs and to improve competitiveness.

We are in a genuine race to avoid being overtaken by other

companies.

Against this backdrop of synergies and cost-reduction,

would you consider modifying your current organization

based on one group, two air carriers, three businesses?

Leo van Wijk